- Your Product Type

- Your Study Type

- Aquatic Ecotoxicology

- Aquatic Invertebrates

- OECD 202: Daphnia sp., Acute Immobilisation Test

- OECD 211: Daphnia magna Reproduction Test

- OECD 235: Chironomus sp., Acute Immobilisation Test

- OECD 218/219: Sediment-Water Chironomid Toxicity Test Using Spiked Sediment/Spiked Water

- OECD 233: Sediment-Water Chironomid Life-Cycle Toxicity Test Using Spiked Water or Spiked Sediment

- OECD 225: Sediment-water Lumbriculus Toxicity Test Using Spiked Sediment

- OECD 242: Potamopyrgus antipodarum Reproduction Test

- OECD 243: Lymnaea stagnalis Reproduction Test

- Fish and other vertebrates

- OECD 203: Fish, Acute Toxicity Test

- OECD 215: Fish Juvenile Growth Study

- OECD 212: Fish, Short-term Toxicity Test on Embryo and Sac-fry Stages

- OECD 231: The Amphibian Metamorphosis Assay

- OECD 236: Fish Embryo Acute Toxicity Test

- OECD 210: Fish, Early-life Stage Toxicity Test

- OECD 229 Fish Short Term Reproduction Assay and OECD 230 21-day Fish Assay

- OECD 240 Medaka Extended One Generation Reproduction Test (MEOGRT)

- OECD 248: Xenopus Eleutheroembryonic Thyroid Assay

- OPPTS 850.1500: Fish Life Cycle Toxicity Test

- OÈCD 234 Fish sexual development test

- Aquatic plants

- Analytical Dose Verification

- Aquatic Invertebrates

- Chemistry

- Biodegradation Studies

- Analytical Chemistry Studies and Residues

- Physical-Chemical Properties Studies

- Storage Stability Studies

- OPPTS 830.6302, OPPTS 830.6303,and OPPTS 830.6304: Physical State, Colour and Odor at 20 °C and at 101.3 kPa

- EU A.1: Melting temperature/range

- EU A.2: Boiling temperature

- EU A.3: Relative density (liquids and solids)

- EU A.4: Vapour pressure

- EU A.5: Surface tension

- EU A.9: Flashpoint

- EU A.10: Flammability (solids)

- EU A.12: Flammability (contact with water)

- EU A.13: Pyrophoric properties of solids and liquids

- EU A.16: Relative self-ignition temperature for solids

- EU A.17: Oxidising properties

- OECD 114: Viscosity of Liquids

- Environmental Fate

- Transformation in Soil

- Transformation in Water

- Transformation in Manure

- Adsorption on Soil and Sewage Sludge

- Bioaccumulation and Bioconcentration

- Terrestrial Ecotoxicology

- Non-target Arthropods

- Non-target arthropod testing with the parasitic wasp (Aphidius rhopalosiphi)

- Non-target arthropod testing with the lacewing (Chrysoperla carnea)

- Non-target arthropod testing with the ladybird beetle (Coccinella septempunctata)

- Non-target arthropod testing with the predatory bug (Orius laevigatus)

- Non-target arthropod testing with the predatory mite (Typhlodromus pyri)

- Non-target arthropod testing with the rove beetle (Aleochara bilineata)

- Non-target arthropod testing with the carabid beetle (Poecilus cupreus)

- Non-target arthropod testing with the wolf spider (Pardosa spec.)

- Soil Organisms

- Honey Bees and other Pollinators

- OECD 213/214: Honey bees, Acute Oral and Acute Contact Toxicity Test

- OECD 245: Honey Bee (Apis Mellifera L.), Chronic Oral Toxicity Test (10-Day Feeding)

- OECD 237: Honey Bee Larval Toxicity Test, Single Exposure

- OECD 239: Honey Bee Larval Toxicity Test

- EPPO 170: Honey Bee Field Study – do plant protection products effect honey bee colonies?

- Oomen et al. 1992: Honey Bee Brood Feeding Study

- OECD 75: Honey Bee Brood Test under Semi-field Conditions in Tunnels

- OECD 246/247 Acute Oral and Contact Toxicity to the Bumblebee, Bombus terrestris L.

- Solitary Bee Acute Contact Toxicity Study in the Laboratory (Osmia sp.) Solitary Bee Acute Oral Toxicity Study in the Laboratory (Osmia sp.) (protocols for ringtests with solitary bees recommended by the non-Apis working group)

- SANTE/11956/2016 rev.9 Residue trials for MRL setting in honey

- Non-target plants

- OECD 208: Terrestrial Plant Test - Seedling Emergence and Seedling Growth Test

- OECD 227: Terrestrial Plant Test - Vegetative Vigour Test

- OCSPP 850.4100: Seedling Emergence and Seedling Growth

- OCSPP 850.4150: Vegetative Vigor

- EPPO PP 1/207(2): Efficacy evaluation of plant protection products, Effects on succeeding crops

- Field Studies

- Non-target Arthropods

- Ecological Modelling

- Quality Assurance

- Testing of Potential Endocrine Disruptors

- Aquatic Ecotoxicology

- News

- Company

- Career

- Contact

Our Certificates

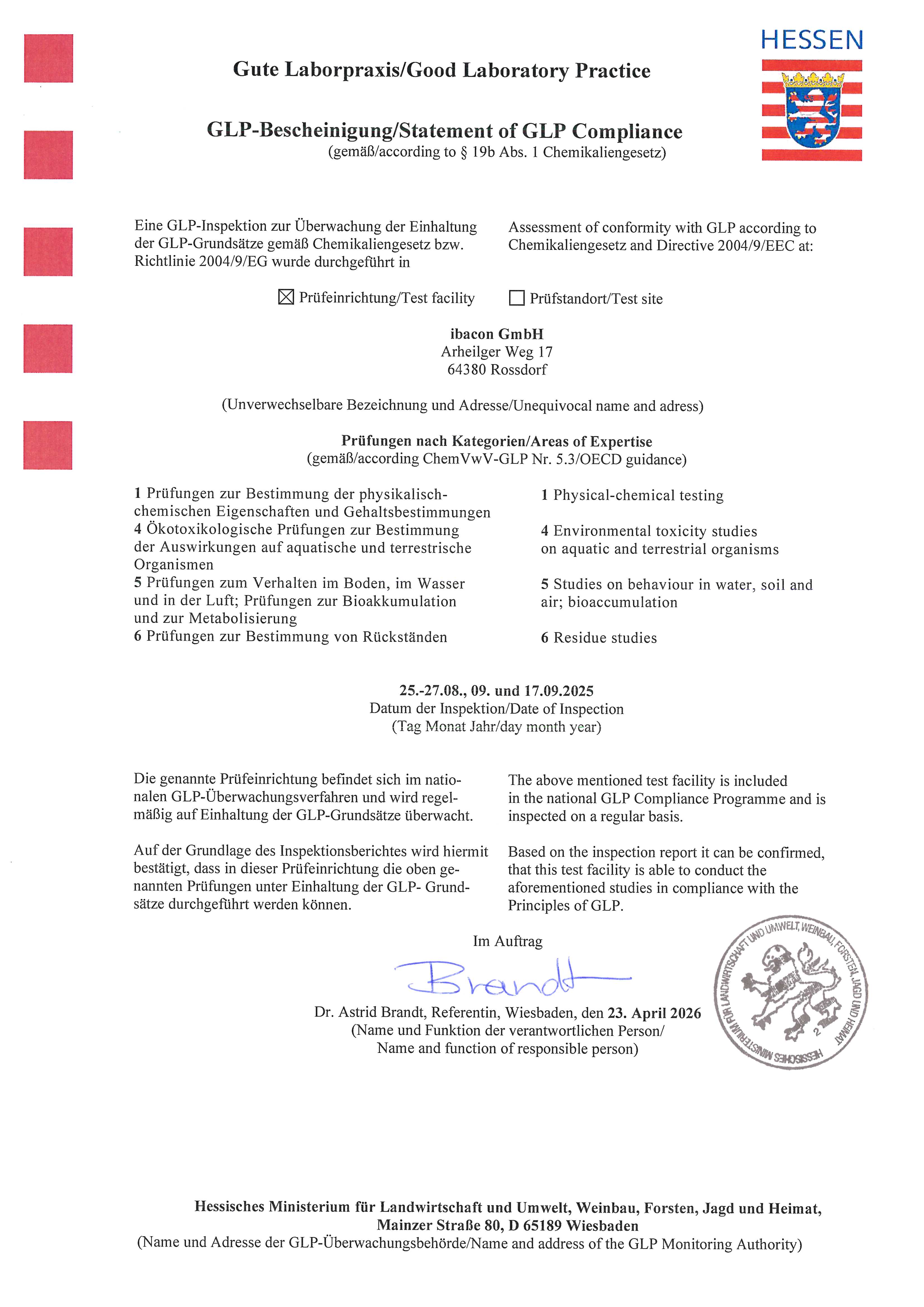

GLP Certificate

The Good Laboratory Pratice or GLP is a quality system for the performance of studies in order to generate high quality test data for the assessment of the safety of chemicals. The OECD Principles of GLP were formally recommended to use in OECD member states in 1981.

The Good Laboratory Pratice or GLP is a quality system for the performance of studies in order to generate high quality test data for the assessment of the safety of chemicals. The OECD Principles of GLP were formally recommended to use in OECD member states in 1981.

The aims of this quality system are to ensure the quality, reliability, reproducibility and integrity of non-clinical chemical safety tests. Studies for the assessment of chemicals need to be performed according to the GLP regulations, otherwise the studies are not accepted in the EU, the United States and many other countries in the world.

The certification according to the "Good Laboratory Practise" is fundamental for our work. Almost all studies are performed according to GLP regulations. ibacon is certified according to the OECD Principles of Good Laboratory Practise since 1995 and the last inspection took place in 2025.

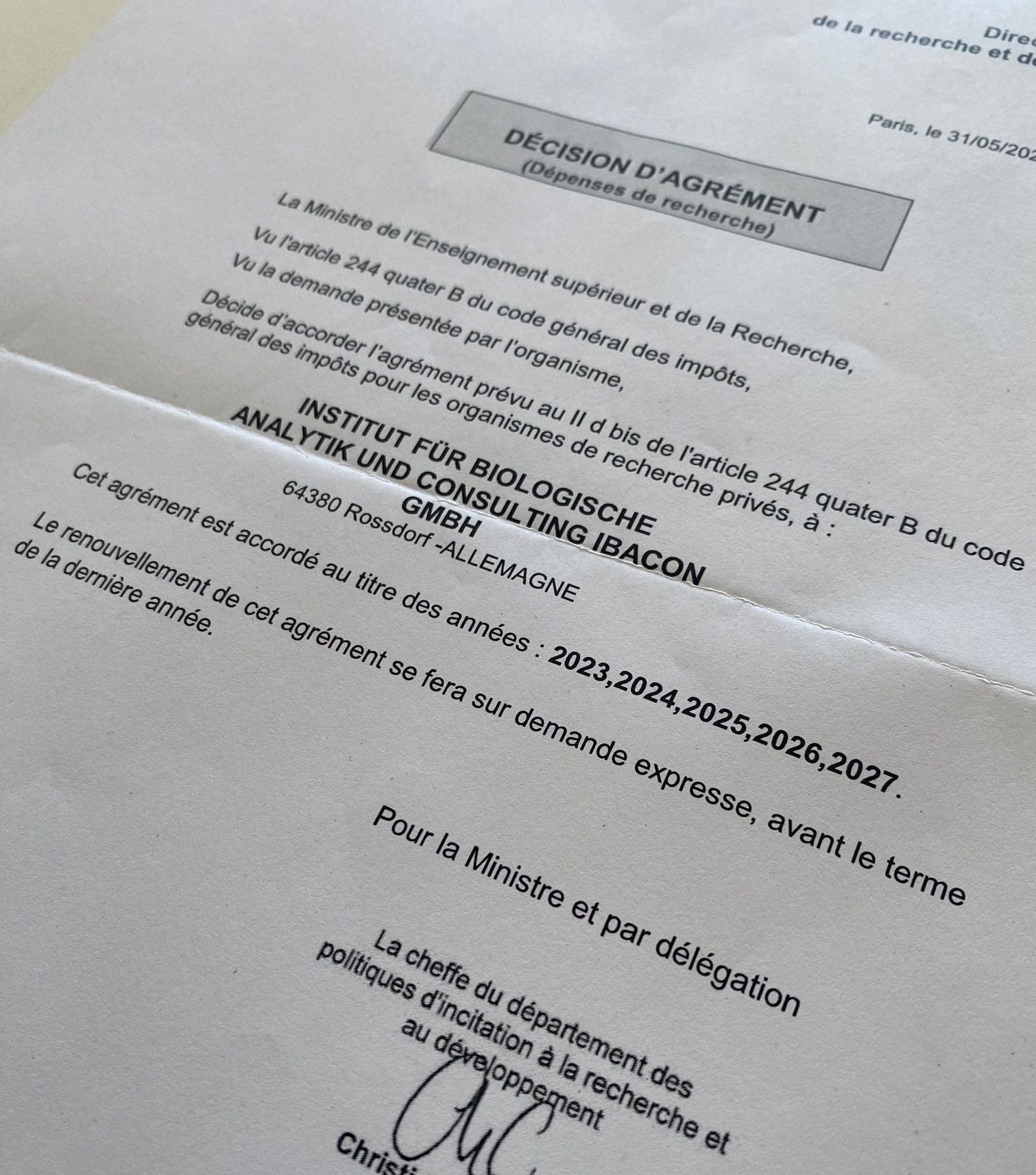

CIR valid until 2027

The "Crédit d’Impôt Recherche" is a tax credit on research expenses for companies that are registered in France. Contract laboratories such as ibacon which conduct studies for these companies need to be certified by the French authorities in order for these tax credits to be granted. ibacon received its first certification in 2006 and has been certified ever since. The certificate is valid until 2027.

We are proud to be able to offer these tax credits to our French customers by placing their research contracts here at ibacon.

Le Crédit d’Impôt Recherche ou CIR est, en France, une réduction d’impôt calculée sur la base de vos dépenses de R&D engagées. Il est déductible de l’impôt sur le revenu ou sur les sociétés, dû par les entreprises au titre de l’année où les dépenses ont été engagées. Il s’agit donc d’une aide fiscale destinée à soutenir et encourager vos efforts de Recherche et Développement, quel que soit votre secteur d’activité, votre taille ou votre organisation. A ce titre, les dépenses de R&D que vous confiez à des organismes ou à des experts individuels situés dans un pays de l'Union européenne sont éligibles à la condition que le tiers soit agréé par le Ministère de l'Éducation nationale, de l'Enseignement supérieur et de la Recherche.

Ceci est donc le cas d’ibacon, qui a obtenu son premier agrément en 2006. La dernière certification en date est valable jusqu’en 2027, et vous permet ainsi de bénéficier d’un crédit d’impôt égal à 30% de vos dépenses éligibles.